Choosing between an FHA loan vs. conventional loan is one of the first big decisions you’ll make as a first-time home buyer — and it can affect everything from your down payment to your monthly payment to how quickly you close. Here’s a clear, side-by-side breakdown to help you decide which one fits your situation.

FHA Loan vs. Conventional Loan: The Quick Answer for First-Time Buyers

- FHA loans are backed by the Federal Housing Administration. They’re built for buyers with lower credit scores, smaller down payments, or higher debt-to-income ratios — which is why they’re so common among first-time buyers.

- Conventional loans aren’t insured by the government. Lenders take on the risk directly, which means stricter qualification standards — but often better long-term value for buyers with strong credit and savings.

Neither loan is “better” across the board. The right one depends on your credit profile, your savings, and how long you plan to stay in the home.

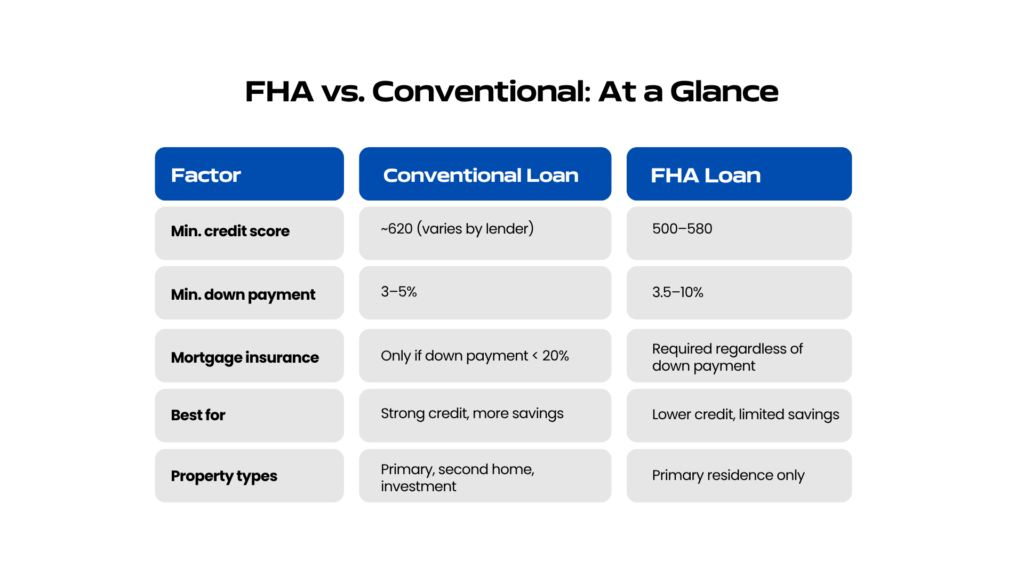

Credit Score Requirements

Conventional loans generally call for a credit score of at least 620, though some lenders look at your full financial picture rather than a hard cutoff.

FHA loans are more forgiving. Most lenders allow a credit score as low as 580 with a 3.5% down payment, and some will go down to 500 with a 10% down payment.

If your credit needs work, an FHA loan keeps the door open while you build it back up. At Quick Mortgage Loans, we help you get there — our team offers credit-improvement guidance and ongoing follow-up so you can track your progress and move toward a conventional loan down the road.

Down Payment Differences

- Conventional: Minimum down payments start around 3–5%, depending on the loan program and whether it’s fixed-rate or adjustable.

- FHA: 3.5% down if your credit score is 580+, or 10% down if your score falls between 500 and 579.

On paper, FHA looks more accessible — but conventional loans with 3% down are increasingly common for first-time buyers who qualify, so it’s worth checking both before assuming FHA is your only option.

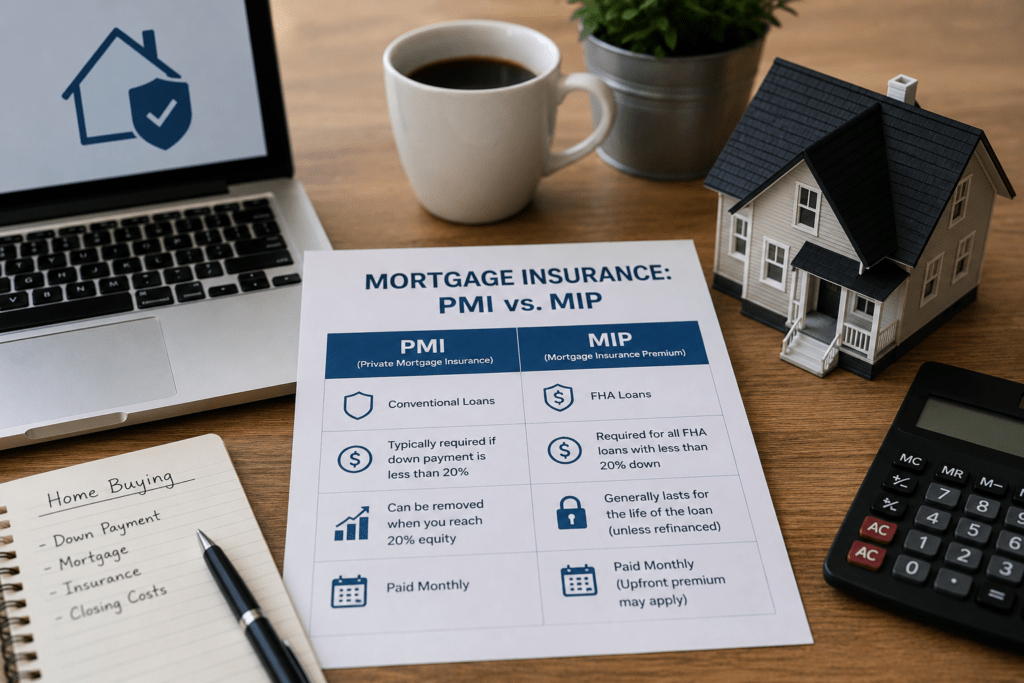

Mortgage Insurance: PMI vs. MIP

This is where the two loan types really diverge.

Conventional PMI only kicks in if your down payment is under 20%. Once you reach 20% equity, you can request to have it removed — and it cancels automatically around 22% equity.

FHA MIP applies no matter how much you put down. You’ll pay an upfront premium (1.75% of the loan amount) plus an annual premium for the life of the loan if your down payment was under 10%. That makes FHA loans more expensive to carry long-term, even if they’re easier to qualify for upfront.

Interest Rates

FHA loans often advertise lower headline interest rates because the government backing reduces lender risk. But once you factor in mandatory mortgage insurance, the effective cost can end up higher than a conventional loan — especially if your credit qualifies you for a competitive conventional rate.

Appraisal Standards

Both loan types require an appraisal, but FHA appraisals are stricter. The home must meet HUD’s minimum property standards — a sound roof and foundation, no exposed wiring, working utilities, and safe access. If a home doesn’t meet those standards, repairs may be required before closing.

This is also why some sellers hesitate to accept FHA-financed offers in competitive markets: the appraisal can surface issues that delay or derail a sale.

Loan Limits

Both FHA and conventional loans have a maximum loan amount, and both vary by county. Conventional conforming loan limits are set annually by the FHFA, and FHA limits are calculated as a percentage of those same figures. If you need to borrow above the conventional limit, you’d be looking at a jumbo loan instead.

Which Should First-Time Buyers Choose?

Choose a conventional loan if:

- Your credit score is in the good-to-excellent range

- You can put down at least 3–5%

- Your debt-to-income ratio is under 45%

- You want the option to drop mortgage insurance later

Choose an FHA loan if:

- Your credit score is below 620

- You have limited savings for a down payment

- Your debt-to-income ratio runs a bit higher

- You’re buying a primary residence (FHA doesn’t cover investment properties)

FAQS

It depends on your credit and savings. Buyers with strong credit and a healthy down payment usually pay less overall with a conventional loan, since they can avoid or cancel mortgage insurance. Buyers with weaker credit may still come out ahead with FHA, since it can be the only path to a competitive rate at all.

Stricter appraisal standards can slow down or complicate a sale, and sellers sometimes worry about financing falling through. In a competitive market, this can put FHA buyers at a slight disadvantage.

Yes. Many homeowners refinance from FHA to conventional once their credit improves and they’ve built enough equity, primarily to eliminate ongoing mortgage insurance premiums.

No. FHA loans are reserved for primary residences. Conventional loans, by contrast, can be used for second homes and investment properties as well.

Not necessarily. FHA is the easier path if your credit or savings aren’t quite there yet, but plenty of first-time buyers qualify for a conventional loan with as little as 3% down — and avoid FHA’s lifelong mortgage insurance in the process. It’s worth getting pre-qualified for both before deciding.

This content is for informational purposes only and does not constitute financial or legal advice. Loan terms and requirements vary by lender.