Buying a home is one of the biggest financial decisions you’ll ever make. Before falling in love with a property, you need to know the answer to one critical question: how much house can you actually afford — and how do you calculate it?

Whether you’re a first-time buyer or looking to upsize, understanding mortgage affordability isn’t just about what the bank will lend you — it’s about what you can comfortably repay for the next 20 to 30 years.

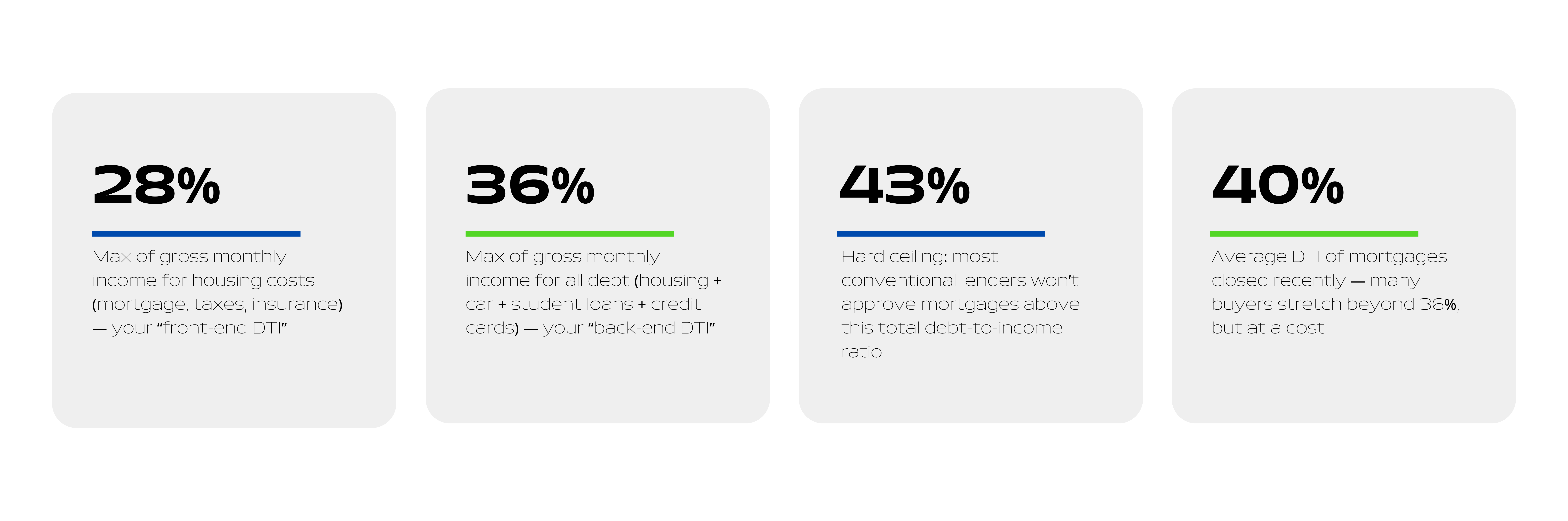

The 28/36 rule: your affordability anchor

Financial experts and mortgage lenders widely use the 28/36 rule as the foundation for deciding how much house you can afford. It’s a rule of thumb, not a hard-and-fast ceiling — but it’s a reliable starting point.

Quick example

If your gross household income is $6,900/month, the 28% rule means your housing costs shouldn’t exceed ~$1,930/month. Apply the 36% ceiling and your total monthly debt (housing + car + credit cards + student loans) should stay under $2,480.

The 28/36 rule is also directly tied to your debt-to-income ratio (DTI). The first number (28%) is your front-end DTI — only housing costs. The second (36%) is your back-end DTI — all monthly debts combined. Lenders focus heavily on back-end DTI when evaluating your mortgage application.

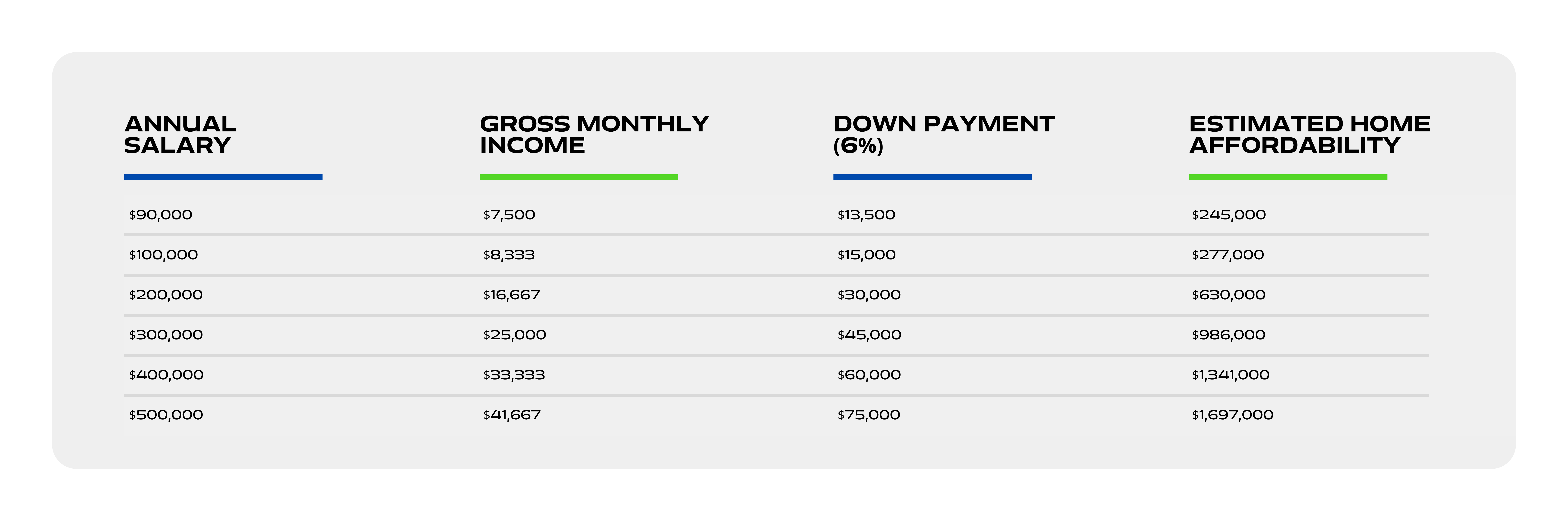

How much house can you afford based on your salary?

The table below provides a general estimate of the maximum home price you may be able to afford based on the 30% housing cost guideline, including estimated property taxes, insurance, and PMI. These figures assume a 6% down payment and reflect U.S. market conditions as a reference benchmark.

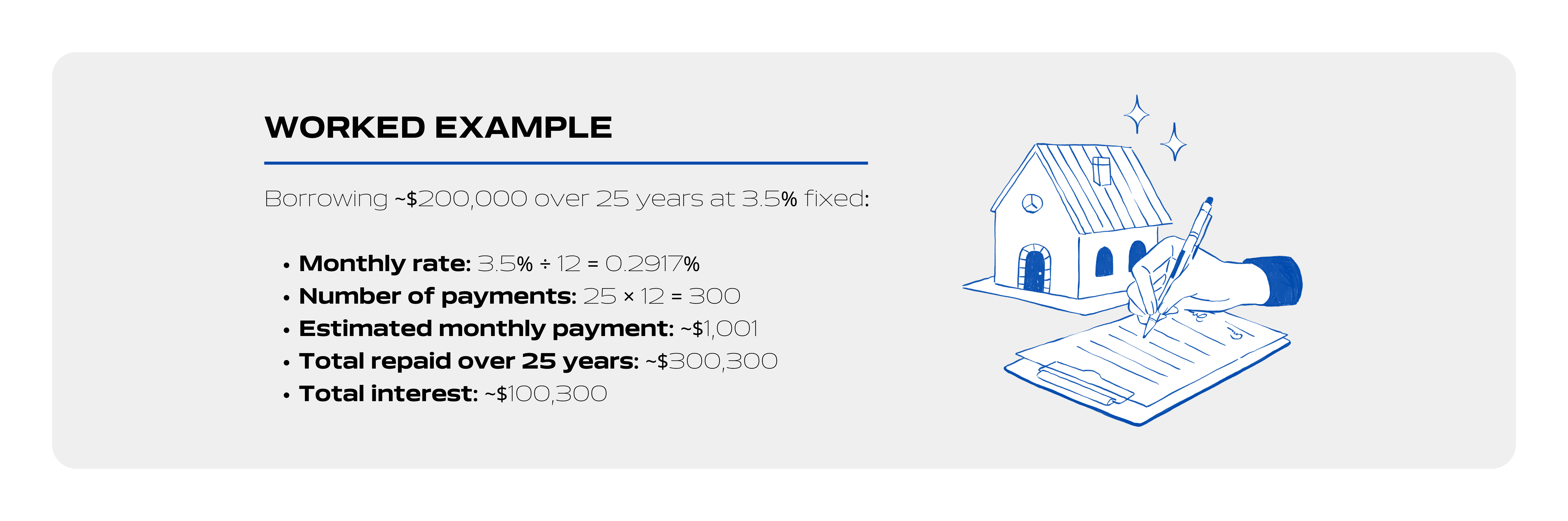

How to calculate your monthly mortgage payment

Your monthly mortgage payment depends on three core variables: the loan amount, the interest rate, and the loan term. Lenders use a standard amortization formula:

Mortgage payment formula

- M = P × [r(1+r)ⁿ] / [(1+r)ⁿ − 1]

M = Monthly payment · P = Principal loan amount · r = Monthly interest rate (annual ÷ 12) · n = Total number of payments (years × 12)

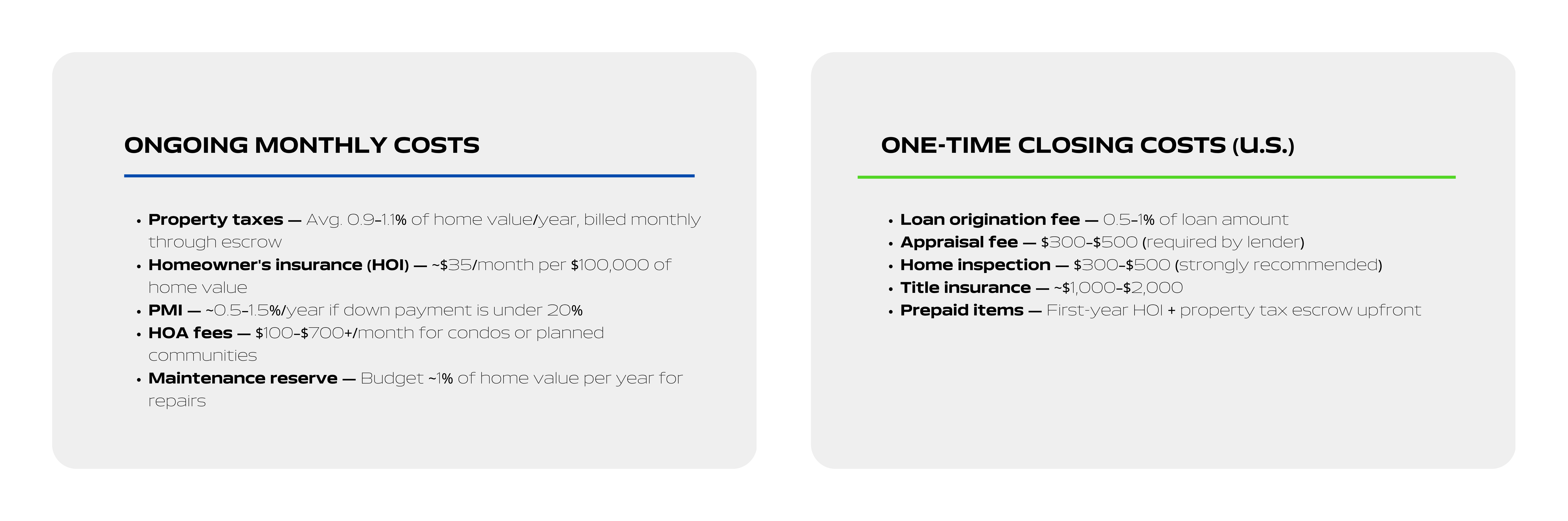

Hidden costs first-time buyers forget

Your monthly mortgage payment covers principal and interest — but the true monthly cost of homeownership in the U.S. is higher. Here’s what first-time buyers routinely underestimate:

How to improve your affordability before applying

If the numbers aren’t quite where you need them to be, here are proven steps to strengthen your position:

- Pay down existing debt — Reducing your credit card balance, car loan, or student debt directly lowers your back-end DTI and can boost your credit score simultaneously.

- Improve your credit score — Pay bills on time, reduce credit utilization below 30%, and avoid new credit applications in the 6–12 months before applying for a mortgage.

- Save a larger down payment — Every extra percentage point reduces your loan amount and monthly payment. Crossing the 20% threshold also eliminates PMI requirements.

- Extend the loan term — Stretching from 20 to 30 years lowers monthly payments (though you’ll pay more interest overall). Useful when cash flow is tight short-term.

- Consider a co-borrower — Adding a co-borrower with income and good credit increases your combined DTI capacity and may unlock better rates.

Final thoughts

The question “how much house can I afford” doesn’t have one universal answer — it depends on your income, savings, existing debts, local market, and personal risk tolerance. By applying the 28/36 rule, understanding the true cost of ownership, and running your numbers through a reliable mortgage calculator, you can arrive at a figure that’s both realistic and sustainable.

The goal isn’t to borrow the maximum the bank will lend you. It’s to find a monthly mortgage payment that leaves room in your budget to live comfortably, build savings, and weather the unexpected.

Ready to See What You Qualify For?

Buying your first home starts with knowing your options. At Quick Mortgage Loans, we help you explore your mortgage possibilities, estimate your monthly payment, and guide you through every step of the process.

Find out how much home you can affordFAQS

You typically need a minimum credit score of 620 for a conventional loan, 580 for an FHA loan (with 3.5% down), or 500 for an FHA loan with 10% down. VA loans have no official minimum but most lenders require 620+.

Plan to save at least 20% for the down payment + 2–5% for closing costs + 3–6 months of mortgage payments as an emergency reserve. On a $300,000 home, that’s roughly $75,000–$90,000 in total savings before you buy.

Pre-qualification is an informal estimate of how much you might borrow, based on self-reported information — no credit check required. Pre-approval is a formal, verified commitment from a lender after reviewing your income, assets, and credit, and carries much more weight with sellers.